Medicare Supplement Plans

Medicare Supplement Plans Demystified

Medicare comprises various "parts," each intricately designed to complement one another and deliver comprehensive coverage. However, discrepancies among the plans can leave individuals facing challenges in certain scenarios or encountering significant out-of-pocket expenses. To bridge these gaps, Medicare Supplement Plans, often referred to as "Medigap" plans, were introduced.

A Medicare Supplement plan, when coupled with Original Medicare, ensures nationwide acceptance and typically offers the lowest out-of-pocket costs with maximum flexibility. However, premium rates are influenced by factors such as age, gender, location, tobacco usage, and household eligibility for discounts, leading to considerable variations among plans and carriers.

Understanding Medicare Supplement Plans

Medicare Supplement Plans step in to cover expenses that Medicare typically passes on to the patient, including deductibles, co-pays, and coinsurance. Following Medicare's payment of its share of expenses, the Supplement plan contributes its portion, potentially covering the remaining balance depending on the plan's specifications.

Types of Medicare Supplement (Medigap) Plans

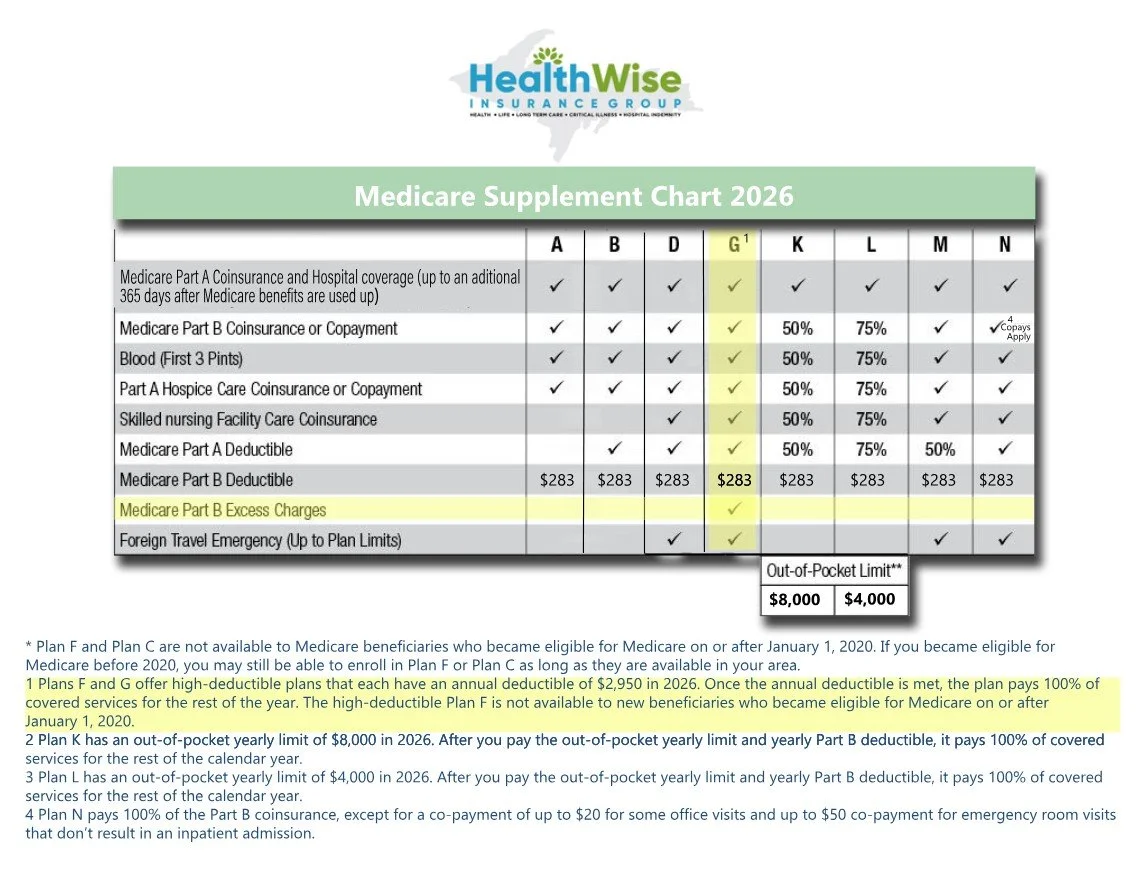

Since 1990, Medicare has standardized Supplement plans, assigning each type a letter from A to N. Regardless of the insurance company, plans sharing the same letter provide identical benefits, differing primarily in premiums. Beneficiaries are advised to compare plans meticulously to find the most suitable one within their budget and needs.

Exclusions from Medicare Supplement Plans

While Medicare Supplement Plans offer comprehensive coverage, they do not include certain items, such as routine dental, hearing, and vision exams, glasses or contacts, hearing aids, retail prescription drugs, or long-term care.

Enrolling in a Medicare Supplement Plan

The Medicare Supplement Open Enrollment Period differs from the Annual Election Period, occurring annually in autumn. Open Enrollment dates vary individually, emphasizing the importance of understanding one's enrollment eligibility.

Key points to note:

Medicare Supplement Open Enrollment is typically a one-time opportunity.

It lasts for six months and is not renewable annually.

Open Enrollment commences on the activation date of Medicare Part B.

Those delaying Part B coverage due to employment will have their Open Enrollment period later when Part B becomes effective.

Eligibility for Medicare before turning 65, due to disability, grants a second Supplement Open Enrollment window upon reaching 65.

Failing to enroll during the six-month window may require answering health questions and undergoing underwriting, potentially leading to coverage denial.

Given the complexity of Medicare Supplement plans, consulting a licensed insurance professional before and during the Open Enrollment period is highly recommended to navigate the process effectively.